As mentioned plenty of times in my market updates regarding the TLT/SPY correlation as a measure of market risk and briefly touched on in my previous article on the notion of bonds as a diversifier in today’s inflationary world, thought I further expand on the implications of a positive stock-bond correlations today!

First of all, whats the stock-bond correlation and how does it affect us? Well, its based on the simple premise that bonds serve as a hedge for equities which has worked fairly well given that this correlation has been persistently negative for the last 20 years. This in turn forms as an important backbone in instituitional portfolio construction or Modern Portfolio Theory (MPT), allowing investors to increase stock allocations while satsifying their risk budgets (Lending → Borrowing).

![FM] Capital Market Line | A Matter of Course](https://substackcdn.com/image/fetch/$s_!7Moi!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Facf8f252-9da6-46b5-a897-bfec99f4f195_585x548.png "FM] Capital Market Line | A Matter of Course")

Aside from perhaps neccesitating the rewriting of CFA textbooks.. the unravelling of this relationship presents a vast amount of risk but before going into them, thought I go through the factors which could cause stock-bond correlations to be postive.

What could cause stock-bond correlations to be positive?

Let’s first dig into the components of both stock and bonds.

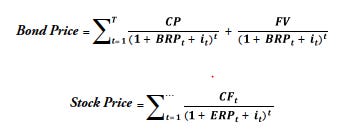

Fundamentally, bond and stock prices reflect the discounted value of all future cash flows. Bonds promise a periodic, fixed nominal coupon payment (CP) and a one-time nominal face-value payment (FV) at maturity. Stocks are a claim on future nominal dividends (CFt). The discount rate is the sum of the nominal risk free rate and respective risk premiums.

The correlation or covariance between the two are then summarised in the equation below:

High Yield Volatility and Inflation

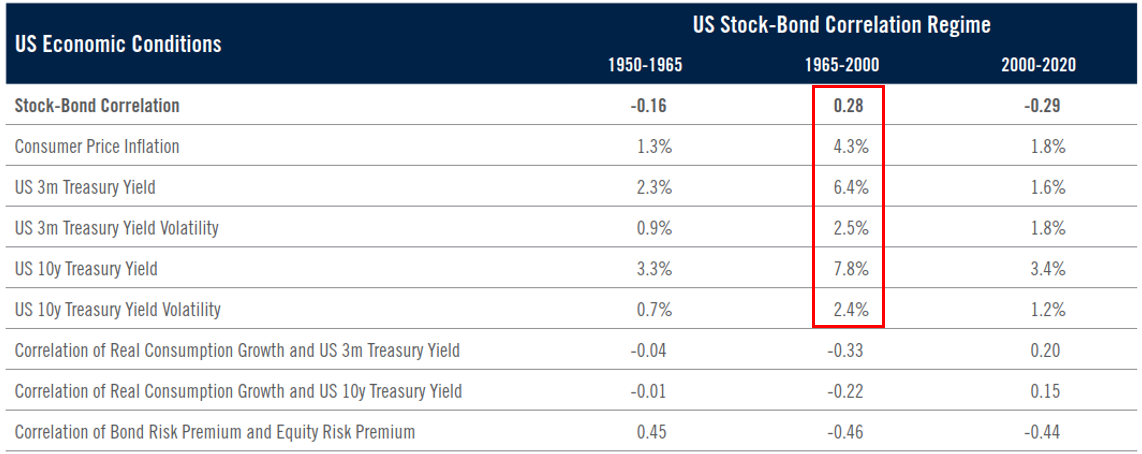

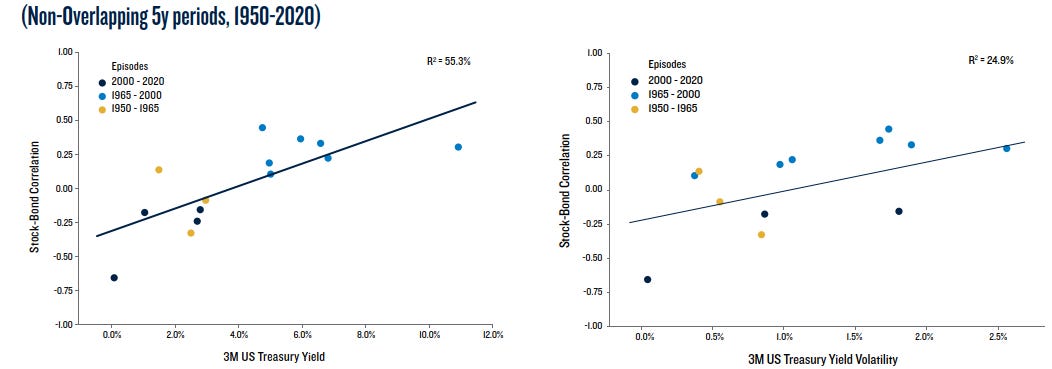

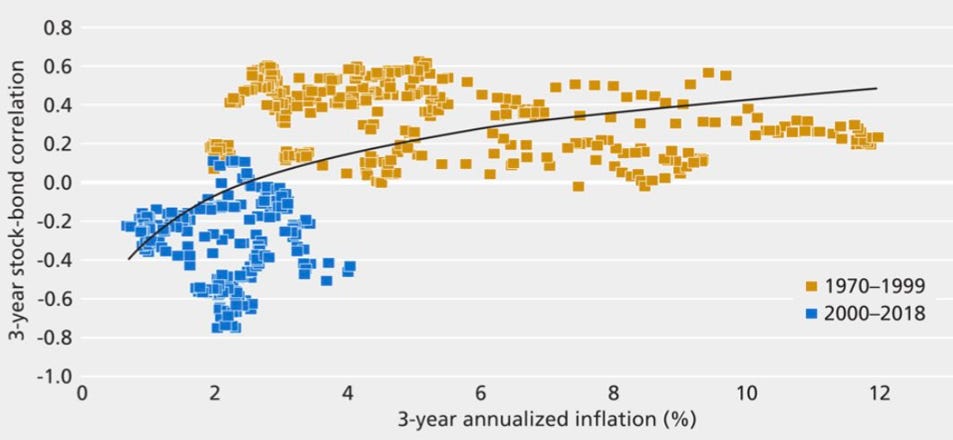

As seen from the equation above, a high volatility in rates generally supports a positive stock-bond correlation as evidenced by the data below.

In addition, periods of high inflation (which is linked to high rates) supports a positive stock-bond correlation as shown in the various data below.

If this doesnt convince you, just look at 2022 1H amidst the inflationary surprises..equities and bonds sold off together!

Restrictive Monetary Policy

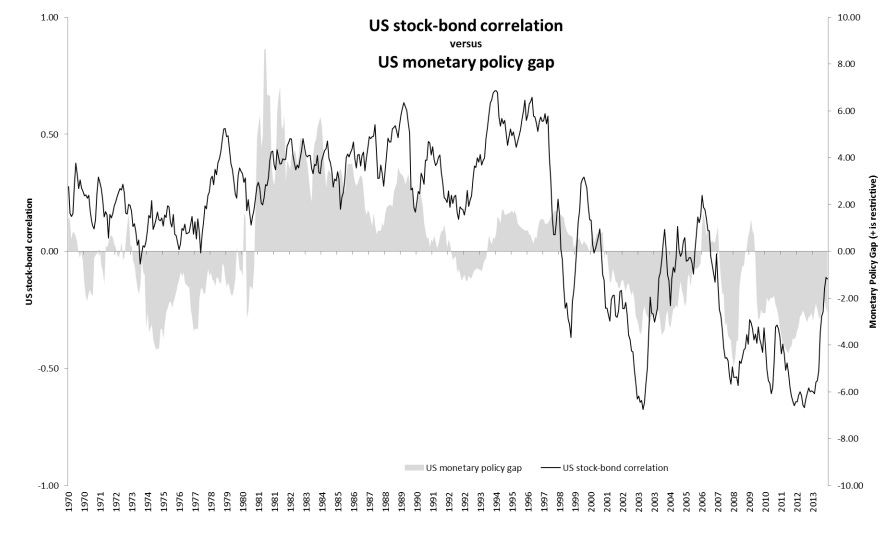

If it isnt apparent from this year’s mantra of rate hiking and the likening of Powell to the late Volcker which has resulted in both equities and bonds selling off toegther…previous periods of restrictive monetary policy have also been supportive of a positive stock-bond correlation as shown below.

Supply Shock

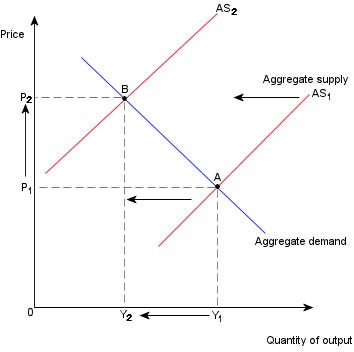

Shifts in aggregate supply are conducive for a positive stock-bond correlations as well. How? Well, lets get back to Econs 101 as demonstrated in the figure below:

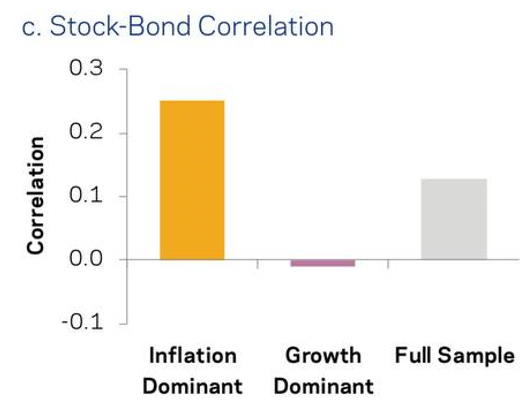

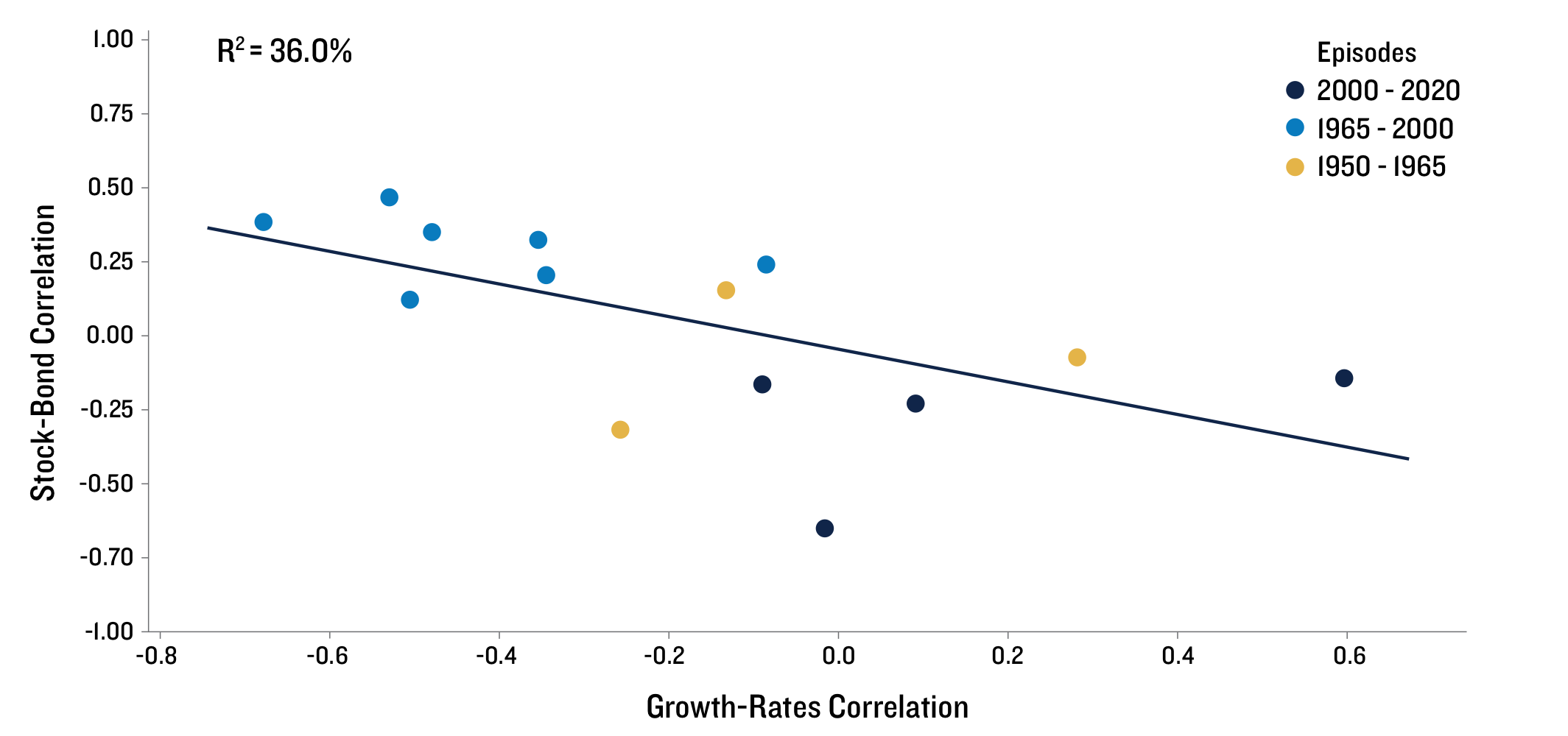

As illustrated in the figure above, an inward shift in aggregate supply would result in a decrease in economic growth while pushing prices up (inflation/rates up). In turn, this contrast between growth and rates (Inflation) perpetuates a positive stock-bond correlation as shown in the data below:

While its understood that theoretical concepts don’t always translate to the real world and shifts in supply are difficult to isolate, the headlines regarding supply chain shocks and high oil prices this year which has in turn resulted in a positive stock-bond correlation so far, is clear evidence that this theory does holds some semblance of validity.

Implications of positive stock-bond correlations

Well aside from destroying the cases for longing bonds as discussed in our previous article, the consequences of a positive stock-bond correlation extends to the general portfolios of financial instituitions as well since lets be honest, most are mere propenents of risk parity ala 60/40..

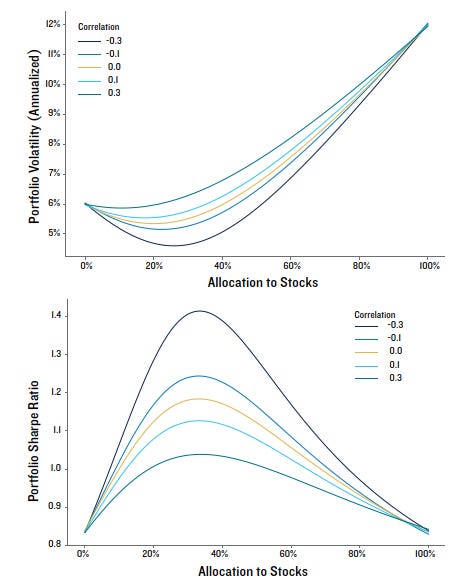

The loss of hedging provided by bonds would result in increased volatility and value-at-risk (VaR) of these portfolios, decreasing their risk-reward profiles. This in turn would force asset allocators to rethink their weightages or more specifically reduce their allocation to stocks to stay within their risk budgets..as shown below.

And just to further extrapolate (if you will allow me!)…in today’s age of passive and systematic flows would this be the cause of the next quant crisis which has always revolved around the crowdedness around a certain assumption.

If 2007 was the quant crisis of long/short strategies and 2018-2020 was the quant crisis of growth factor dominance, are we likely to see the quant crisis of stock-bond correlations unravelling in the near future?

Conclusion

While I am certainly not calling for stock-bond correlations to be persistently positive in the future and for a doomsday scenario of everything down, the implications of correlations unravelling certainly needs to be taken note of as 1H 2022 has already given us a preview of…especially in a period of high & persistent inflation along with a Fed’s stance of tighter for longer.

More importantly, next time when somebody says diversify into fixed income as a hedge for downside… you could perhaps give a second thought!