Market Update 08/15-08/19

Gamma Squeezes are Back! (Blood Bath & Beyond), Inflation Soars in Europe, Housing Slowing

Overview:

Market Recap

What Happened in Macro this Week?

What Lies Ahead

Lets dig into the deets 📊!

Market Overview

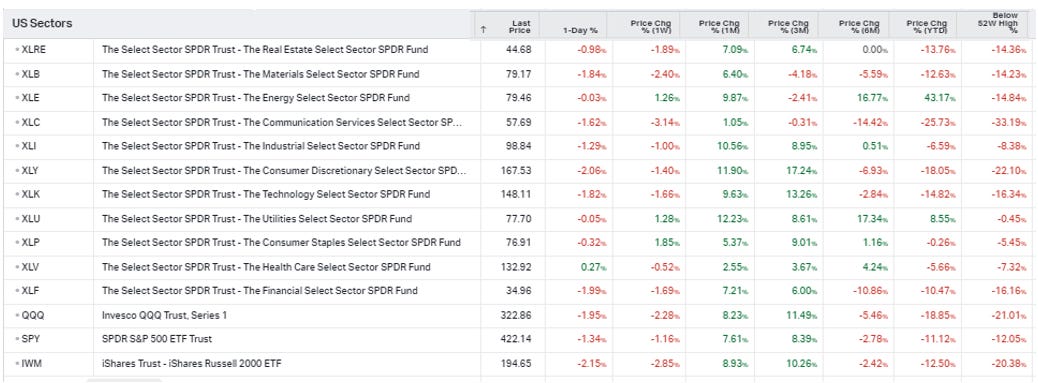

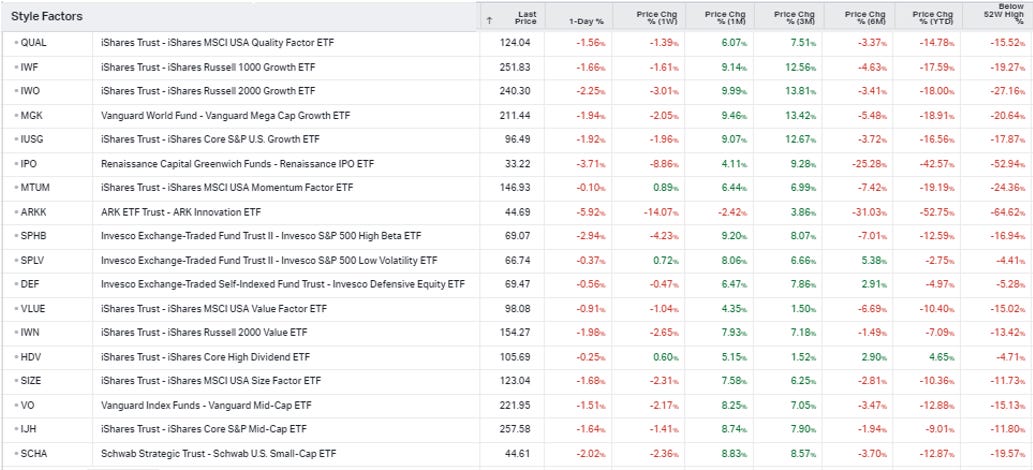

Indices, Sectors & Style Factors

Equities had their bullish streak broken by heavy selling late in the week or as one would term as a window of weakness especially during option expiry week.

Worries largely were perhaps attributed to the global inflationary fears and Jackson Hole next week. The lone exceptions however were Energy and Defensives.

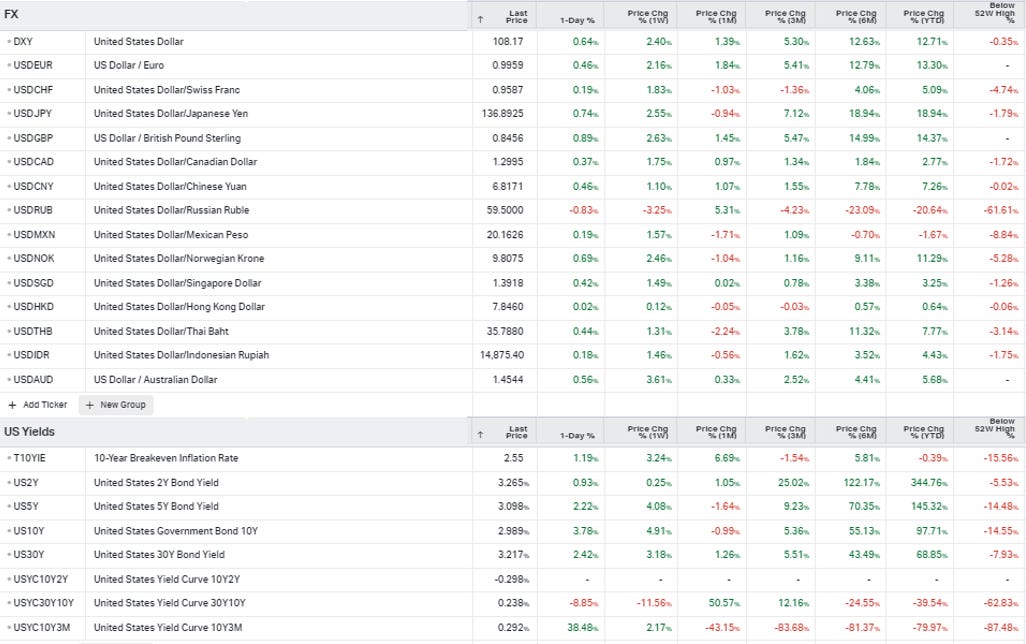

Fixed Income & Foreign Currencies

Yields continued upon their ascent as European data highlight that inflation may not entirely be over. With the recent rally largely being attributed to the collapse in 10Y yields, is this ascent back to ~3% signaling that this rally is near its end? The inverted 10/2’s continues to be negative.

Likewise for the US dollar which is often see as a barometer for risk off action, is its recent strength again signaling that one should expect some selling in the near term?

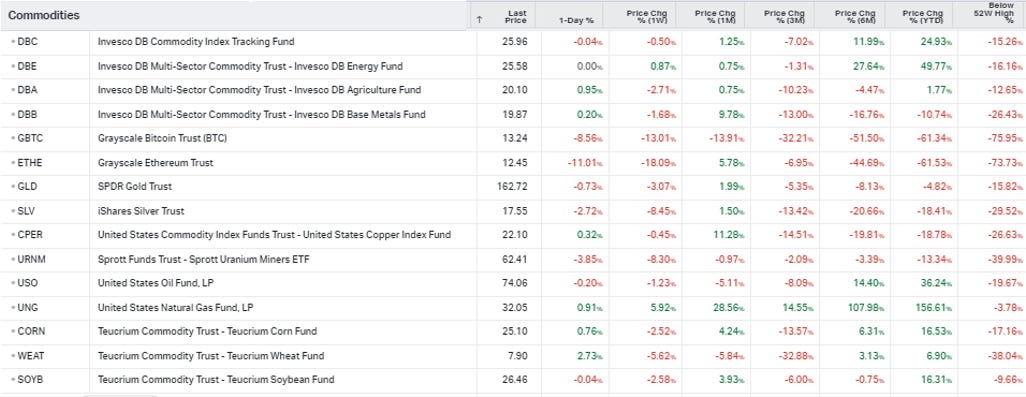

Commodities

Commodities were down on the week with the exception of energy as Natural gas showed again why its the widowmaker..

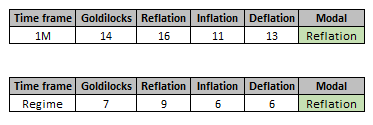

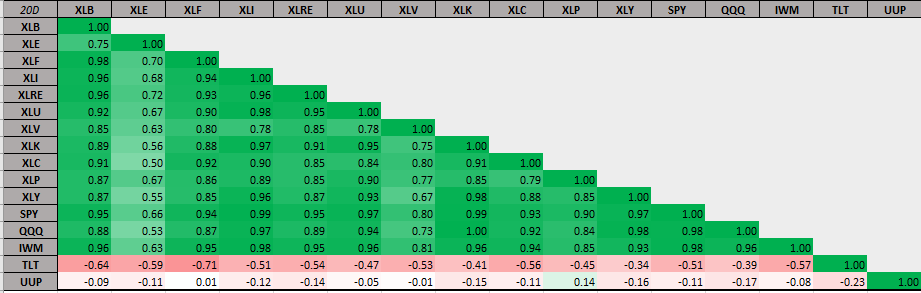

Overall Market Indicators

From a regime/pricing perspective, we remain in a risk on environment but with the low conviction scores from a regime perspective and us entering into a window of weakness on the backdrop of various catalysts (Jackson Hole) next week, it could easily change!

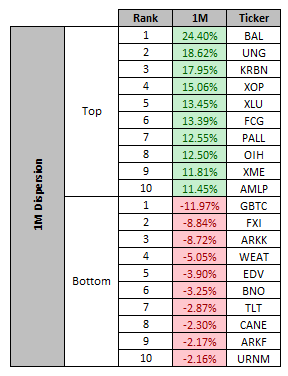

On the dispersion front, the theme of commodites over rate sensitivity highlights again that perhaps inflation hasnt yet peaked. The underperformance of crypto which tends to lead sell offs isnt particularly encouraging as well!

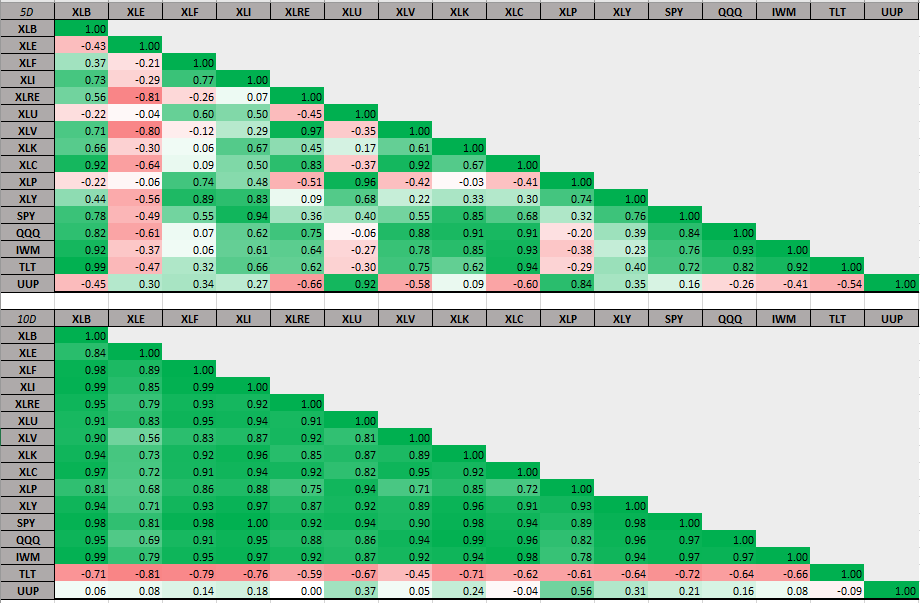

On the correlation front, TLT/SPY correlation is now heavily postive on a 5D basis, a stark contrast to the 10D/20D signals. Hence, it may be prudent to excercise some caution early into next week.

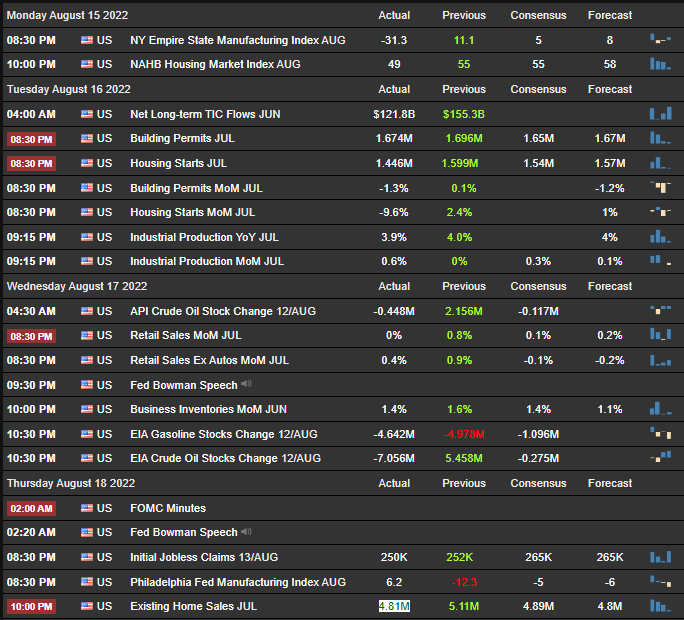

What Happened in Macro this Week

On the macro front, the data continues to emphasize the theme that growth is slowing:

The deccelerations on the housing front (NAHB,Building Permits & Housing Starts) points to further slowing for the broader economy ahead as housing generally tends to be a leading indicator for the economic activity.

The retail sales on the other hand which beat consensus highlights the case whereby we maybe in a goldilocks environment where the slow down in Inflation outpaces that of growth.

On the global front, there is growing evidence that inflation may not be quite over as the bond market this week may atest to:

CPI in the UK soared to a 2-handle of 10.1%, beating consensus

German PPI which tends to lead CPI soared to +5.3%, consensus was +0.6% (Yes! It isnt a typo)

China announces rate cuts in a bid to stimulate its economy which has been dire as of late (Not quite the recovery many were hoping for a few months ago…). How this Chinese Easing vs US Tightening dynamic plays out would definitely be something to keep an eye on w.r.t inflation in the US

On the company front :

Sea posted a net loss of $931 million which worsened from $433 million a year ago. Profitability is increasingly becoming a priority as they promise cost cuts, pausing guidance citing “volatility”.

Bed, Bath & Beyond squeezed this week on news of Ryan Cohen’s involvement ($1.67 mil deep OTM calls), reminienscent of the meme stock mania back in 2020… ( Are we on the cusp of a new bull market ala 2020?)

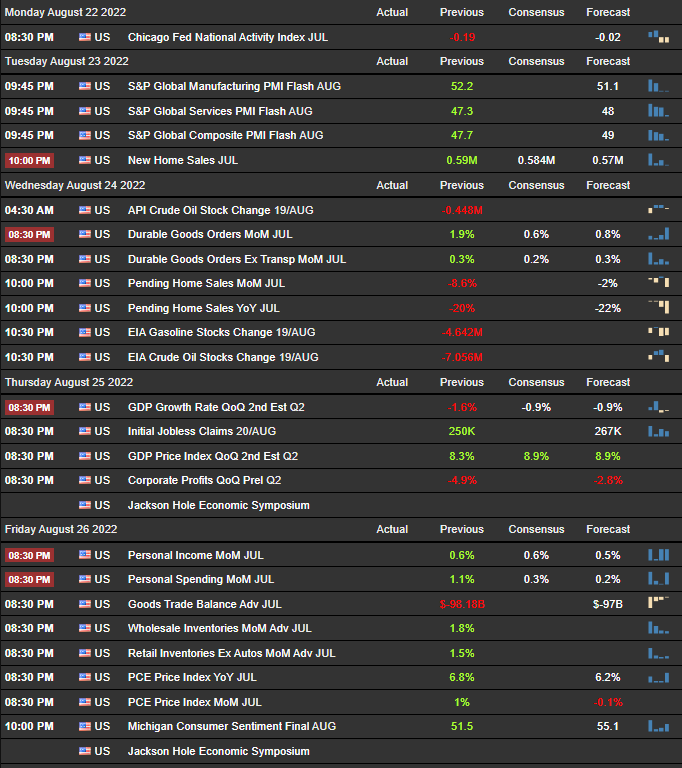

What Lies Ahead

Economic Calendar

Earnings Calendar

Looking to be a moderate earnings but economic heavy week (Jackson Hole!). With us being in a window of weakness as mentioned, definitely would be a time for caution..⚠️

Till next time, stay safe and be liquid 💦!